The first thing you do is recreate the conditions that preceded the last one:

I hope I don't end up making angry "I told you so" posts. Because that will mean the wheels have fallen off.

Actions by federal regulators and Republicans in Congress over the past two years have paved the way for banks and other financial companies to issue more than $1 trillion in risky corporate loans, sparking fears that Washington and Wall Street are repeating the mistakes made before the financial crisis.

The moves undercut policies put in place by banking regulators six years ago that aimed to prevent high-risk lending from once again damaging the economy.

Now, regulators and even White House officials are struggling to comprehend the scope and potential dangers of the massive pool of credits, known as leveraged loans, they helped create.

Goldman Sachs, Wells Fargo, JP Morgan Chase, Bank of America and other financial companies have originated these loans to hundreds of cash-strapped companies, many of which could be unable to repay if the economy slows or interest rates rise.

“This means that the next downturn that we have could be more serious and longer-lasting and more difficult to deal with than it would have been if we had constrained these practices,” former Federal Reserve chair Janet L. Yellen said in an interview.

The lending boom was precipitated, in part, by the rush to water down regulations at the start of the Trump administration. That’s when newly minted regulators — many with close ties to the financial industry — sought to strip away post-crisis financial rules and find ways to juice the economy by encouraging more lending.

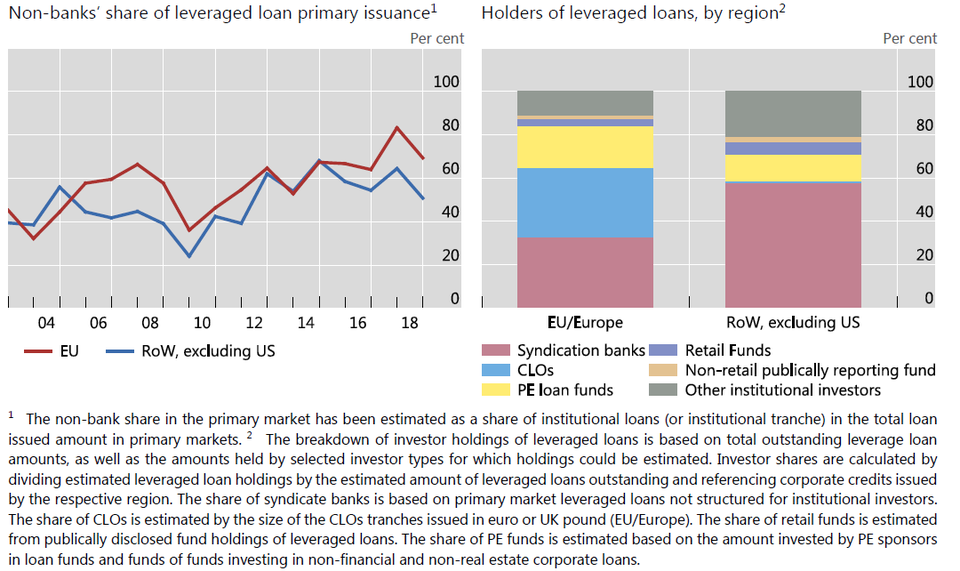

One of their top targets was leveraged loans. These are giant loans that banks make to heavily indebted — in financial speak, highly leveraged — companies. Bankers often have little assurance that the loans can be repaid, which can make them particularly risky. Bankers earn large fees off these products, and many banking executives say their institutions are sheltered from losses because they sell the loans to other investors such as hedge funds, mutual funds and insurance companies.

This should worry anyone who's familiar with the causes of the 2008 financial crisis:The moves undercut policies put in place by banking regulators six years ago that aimed to prevent high-risk lending from once again damaging the economy.

Now, regulators and even White House officials are struggling to comprehend the scope and potential dangers of the massive pool of credits, known as leveraged loans, they helped create.

Goldman Sachs, Wells Fargo, JP Morgan Chase, Bank of America and other financial companies have originated these loans to hundreds of cash-strapped companies, many of which could be unable to repay if the economy slows or interest rates rise.

“This means that the next downturn that we have could be more serious and longer-lasting and more difficult to deal with than it would have been if we had constrained these practices,” former Federal Reserve chair Janet L. Yellen said in an interview.

The lending boom was precipitated, in part, by the rush to water down regulations at the start of the Trump administration. That’s when newly minted regulators — many with close ties to the financial industry — sought to strip away post-crisis financial rules and find ways to juice the economy by encouraging more lending.

One of their top targets was leveraged loans. These are giant loans that banks make to heavily indebted — in financial speak, highly leveraged — companies. Bankers often have little assurance that the loans can be repaid, which can make them particularly risky. Bankers earn large fees off these products, and many banking executives say their institutions are sheltered from losses because they sell the loans to other investors such as hedge funds, mutual funds and insurance companies.

One reason bankers have been able to make so many of these higher-risk loans without regulatory interference is that they sell these products on to outside investors. The loans are packaged into products known as collateralized loan obligations, or CLOs.

The CLO market has surged in the past 10 years, growing from $300 billion at the end of 2008 to $615 billion at the end of 2018, but the quality of these products is worse than it was before the financial crisis, according to the Federal Reserve Bank of Dallas.

Some former regulators have noted an eerie parallel between the subprime mortgage crisis and the leveraged-loan buildup. In the 2000s, banks and other finance companies took risky loans — certain mortgages — and packaged them into products that were sold off to investors. Financial companies also made other exotic instruments, known as collateralized debt obligations, tied to those securities. The products entangled financial companies with one another, allowing weak institutions to pull down stronger institutions when the value of these products cratered.

Today, regulators say they don’t have a firm grip on what the impact will be when the economy weakens or enters a recession.

Meanwhile, Trump is trying to turn the Fed's board of governors into a clown show. As noted in the piece above:The CLO market has surged in the past 10 years, growing from $300 billion at the end of 2008 to $615 billion at the end of 2018, but the quality of these products is worse than it was before the financial crisis, according to the Federal Reserve Bank of Dallas.

Some former regulators have noted an eerie parallel between the subprime mortgage crisis and the leveraged-loan buildup. In the 2000s, banks and other finance companies took risky loans — certain mortgages — and packaged them into products that were sold off to investors. Financial companies also made other exotic instruments, known as collateralized debt obligations, tied to those securities. The products entangled financial companies with one another, allowing weak institutions to pull down stronger institutions when the value of these products cratered.

Today, regulators say they don’t have a firm grip on what the impact will be when the economy weakens or enters a recession.

Last year, partly at the urging of Powell, the White House nominated economist and financial-regulation expert Nellie Liang to the central bank’s Board of Governors.

Her nomination from the White House was exceptional, in that she does not have a banking background and previously worked at the Fed to fine-tune oversight of financial companies. She formerly directed the Federal Reserve’s Office of Financial Stability, one of its most powerful components.

Banking industry lobbyists whipped up opposition to Liang, persuading some Republicans on the Senate Banking Committee to block her confirmation, according to five people involved in the process. In January, she announced she was withdrawing from consideration after it became clear she could not win Senate confirmation.

Instead of Liang, Trump reportedly is nominating Stephen Moore and Herman Cain -- a couple of kooks and grifters who shouldn't be allowed into the Federal Reserve on a visitor's pass. But they'll congenially try to do whatever President Dunning-Kruger wants done, so Senate Republicans may well confirm them.Her nomination from the White House was exceptional, in that she does not have a banking background and previously worked at the Fed to fine-tune oversight of financial companies. She formerly directed the Federal Reserve’s Office of Financial Stability, one of its most powerful components.

Banking industry lobbyists whipped up opposition to Liang, persuading some Republicans on the Senate Banking Committee to block her confirmation, according to five people involved in the process. In January, she announced she was withdrawing from consideration after it became clear she could not win Senate confirmation.

I hope I don't end up making angry "I told you so" posts. Because that will mean the wheels have fallen off.